Post by Sapphire Capital on Sept 10, 2012 21:15:48 GMT 4

Morris Trust

Basic Principles

A "Morris Trust" or "reverse Morris Trust" transaction is an M&A technique for a company to effectuate a sale of a division or divisions to a Buyer without incurring any corporate tax in the transaction

In a Morris Trust, all assets other than those being acquired are spun off into a new public company, with the remaining assets being merged with the Buyer. In a reverse Morris Trust ("RMT"), the assets to be acquired are spun off and promptly merged with the Buyer

The reverse Morris Trust format is currently much more common than the Morris Trust format as it typically provides the most direct means to effectuate the transaction

The reverse Morris Trust and Morris Trust structures can also be executed as split-offs as well as spin-offs

The March 2007 Weyerhaeuser/Domtar transaction is the first reverse Morris Trust executed as a split-off; structure can be attractive as a means to ensure that shares are placed in the right hands

Key structuring issues:

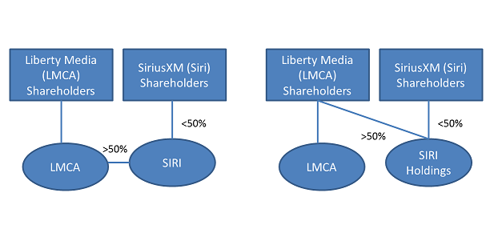

50% Requirement: Shareholders of Seller must receive over 50% of the vote and value of the surviving entity in the merger (the "50% Test"). For purposes of this requirement, shares in the pro forma company owned by the Seller shareholders by virtue of equity positions in the Buyer are generally counted under the Shareholder Overlap rules.

Equity Financing: Dilution of Seller shareholders by planned post-transaction equity issuances by the surviving entity will be counted for purposes of the "50% Test". Equity issuances within a 2-year period of the transaction may be treated as "planned" for this purpose

Monetization Possible: The debt/equity and debt/debt swap techniques described under Monetizing Spin-Offs are equally available to Seller here and have been utilized in numerous such transactions ruled upon by the IRS. However, such strategies will reduce the percentage of the merged entity owned by historic Seller shareholders, putting pressure on the 50% Test (see Heinz/Del Monte)

Post-Merger M&A: Under the revised Morris Trust rules, as long as the Seller and potentially the Buyer have not had significant M&A discussions with a Target for the 2 years preceding the spin, the combined entity can commence M&A dialogue with respect to the Target promptly after the closing of the Morris Trust transactions. If such discussions have occurred, a 6-month or 1-year wait may be required. A similar analysis applies to M&A dialogue by the Seller, although the Seller will have greater "cushion" on the 50% Test due to the absence of any change in shareholder base in the transaction

Corporate Governance: Notwithstanding the 50% requirement, the Buyer in a Morris Trust acquisition can retain effective control over the Board of Directors and senior management of the surviving entity (see P&G/J.M. Smucker and Mariner/Forest Oil)

Precedent transactions: FairPoint/Verizon, Alltel/Valor, Weyerhaeuser/Domtar, Forest Oil/Mariner, Heinz/Del Monte, JIF/J.M. Smucker, AT&T Broadband/Comcast

Corporate Governance

The principal tax requirement is that the Seller shareholders receive greater than 50% of the vote and value of the pro forma company, as per Section 355(e)

In the RMT context, the IRS has not typically required that this greater-than-50% vote be reflected in any initial or future composition of the Board or Management of the pro forma Company, as long as (i) the Board is elected through normal shareholder voting going forward, and (ii) the normal powers of the Board over major corporate decisions are respected going forward

As the chart below shows, in several recent deals the Board and senior management of the Buyer have dominated the governance of the pro forma company on a going-forward basis (although there is also precedent where the Seller has predominated)

Based on these precedents, the Buyer should have significant flexibility from a tax perspective to have the Board and senior management of its choice, notwithstanding the Section 355(e) requirements around shareholder ownership

Any mechanisms put into place which could mitigate the impact of the Seller shareholder voting rights (unusually long Board terms, limits on ability of Board to control major corporate decisions, appoint senior management, etc.) will, however, be carefully scrutinized by the IRS

In some deals (e.g. AT&T Broadband/Comcast), the Buyer shareholders have obtained the right to a special class vote over major corporate transactions

Such mechanisms would be permissible for tax purposes if they are limited to transactions which would normally come to a shareholder vote (e.g. large-scale M&A, amendments of the charter, etc.)

While such provisions do give Buyer greater control going forward, they do also imply having two classes of public securities.

Transaction Structure - RMT

Step 1 Transaction Steps

P signs a contract to sell S to Buyer

Closing condition to acquisition that P spin-off S

Step 2 Transaction Steps

P spins off S, which merges with Buyer

If monetizing spin-off technology utilized, S dropped into NewCo to facilitate debt/equity, debt/debt swap

Transaction Structure - RMT with Debt-for-Debt Exchange

Step 1 - Formation of NewCo

ParentCo contributes assets and debt up to its tax basis in the wanted assets to a NewCo in exchange for NewCo equity and notes

Step 2 - Debt-for-Debt Exchange

Investment Bank buys ParentCo debt in open market

ParentCo delivers NewCo Notes to Investment Bank in exchange for ParentCo debt in a debt-for-debt swap; Investment Bank sells NewCo Notes to investors

Step 3 - NewCo Merges with InvestorCo

Transaction Structure - Morris Trust

Step 1 Transaction Steps

P enters into contract to sell S2 to Buyer

Closing condition that P first spin off S1

Step 2 Transaction Steps

P spins off S1 and then merges with Buyer

If monetizing spin-off technology to be utilized, P drops S1 into NewCo to facilitate debt/equity, debt/debt swaps

Advantages & Disadvantages

Advantages

Permanently tax-free disposition of business

Significant monetization possible through debt/equity, debt/debt swaps

Shareholders get benefits of synergies of merger and, potentially, a control premium

Buyer can retain effective control of Board of Directors and senior management of surviving entity, notwithstanding Section 355 requirements

Disadvantages

Monetization limited by market capacity and Section 355 limitations

Limited universe of merger partners due to Section 355 requirement

Post-transaction equity issuance may be limited under Section 355

Basic Principles

A "Morris Trust" or "reverse Morris Trust" transaction is an M&A technique for a company to effectuate a sale of a division or divisions to a Buyer without incurring any corporate tax in the transaction

In a Morris Trust, all assets other than those being acquired are spun off into a new public company, with the remaining assets being merged with the Buyer. In a reverse Morris Trust ("RMT"), the assets to be acquired are spun off and promptly merged with the Buyer

The reverse Morris Trust format is currently much more common than the Morris Trust format as it typically provides the most direct means to effectuate the transaction

The reverse Morris Trust and Morris Trust structures can also be executed as split-offs as well as spin-offs

The March 2007 Weyerhaeuser/Domtar transaction is the first reverse Morris Trust executed as a split-off; structure can be attractive as a means to ensure that shares are placed in the right hands

Key structuring issues:

50% Requirement: Shareholders of Seller must receive over 50% of the vote and value of the surviving entity in the merger (the "50% Test"). For purposes of this requirement, shares in the pro forma company owned by the Seller shareholders by virtue of equity positions in the Buyer are generally counted under the Shareholder Overlap rules.

Equity Financing: Dilution of Seller shareholders by planned post-transaction equity issuances by the surviving entity will be counted for purposes of the "50% Test". Equity issuances within a 2-year period of the transaction may be treated as "planned" for this purpose

Monetization Possible: The debt/equity and debt/debt swap techniques described under Monetizing Spin-Offs are equally available to Seller here and have been utilized in numerous such transactions ruled upon by the IRS. However, such strategies will reduce the percentage of the merged entity owned by historic Seller shareholders, putting pressure on the 50% Test (see Heinz/Del Monte)

Post-Merger M&A: Under the revised Morris Trust rules, as long as the Seller and potentially the Buyer have not had significant M&A discussions with a Target for the 2 years preceding the spin, the combined entity can commence M&A dialogue with respect to the Target promptly after the closing of the Morris Trust transactions. If such discussions have occurred, a 6-month or 1-year wait may be required. A similar analysis applies to M&A dialogue by the Seller, although the Seller will have greater "cushion" on the 50% Test due to the absence of any change in shareholder base in the transaction

Corporate Governance: Notwithstanding the 50% requirement, the Buyer in a Morris Trust acquisition can retain effective control over the Board of Directors and senior management of the surviving entity (see P&G/J.M. Smucker and Mariner/Forest Oil)

Precedent transactions: FairPoint/Verizon, Alltel/Valor, Weyerhaeuser/Domtar, Forest Oil/Mariner, Heinz/Del Monte, JIF/J.M. Smucker, AT&T Broadband/Comcast

Corporate Governance

The principal tax requirement is that the Seller shareholders receive greater than 50% of the vote and value of the pro forma company, as per Section 355(e)

In the RMT context, the IRS has not typically required that this greater-than-50% vote be reflected in any initial or future composition of the Board or Management of the pro forma Company, as long as (i) the Board is elected through normal shareholder voting going forward, and (ii) the normal powers of the Board over major corporate decisions are respected going forward

As the chart below shows, in several recent deals the Board and senior management of the Buyer have dominated the governance of the pro forma company on a going-forward basis (although there is also precedent where the Seller has predominated)

Based on these precedents, the Buyer should have significant flexibility from a tax perspective to have the Board and senior management of its choice, notwithstanding the Section 355(e) requirements around shareholder ownership

Any mechanisms put into place which could mitigate the impact of the Seller shareholder voting rights (unusually long Board terms, limits on ability of Board to control major corporate decisions, appoint senior management, etc.) will, however, be carefully scrutinized by the IRS

In some deals (e.g. AT&T Broadband/Comcast), the Buyer shareholders have obtained the right to a special class vote over major corporate transactions

Such mechanisms would be permissible for tax purposes if they are limited to transactions which would normally come to a shareholder vote (e.g. large-scale M&A, amendments of the charter, etc.)

While such provisions do give Buyer greater control going forward, they do also imply having two classes of public securities.

Transaction Structure - RMT

Step 1 Transaction Steps

P signs a contract to sell S to Buyer

Closing condition to acquisition that P spin-off S

Step 2 Transaction Steps

P spins off S, which merges with Buyer

If monetizing spin-off technology utilized, S dropped into NewCo to facilitate debt/equity, debt/debt swap

Transaction Structure - RMT with Debt-for-Debt Exchange

Step 1 - Formation of NewCo

ParentCo contributes assets and debt up to its tax basis in the wanted assets to a NewCo in exchange for NewCo equity and notes

Step 2 - Debt-for-Debt Exchange

Investment Bank buys ParentCo debt in open market

ParentCo delivers NewCo Notes to Investment Bank in exchange for ParentCo debt in a debt-for-debt swap; Investment Bank sells NewCo Notes to investors

Step 3 - NewCo Merges with InvestorCo

Transaction Structure - Morris Trust

Step 1 Transaction Steps

P enters into contract to sell S2 to Buyer

Closing condition that P first spin off S1

Step 2 Transaction Steps

P spins off S1 and then merges with Buyer

If monetizing spin-off technology to be utilized, P drops S1 into NewCo to facilitate debt/equity, debt/debt swaps

Advantages & Disadvantages

Advantages

Permanently tax-free disposition of business

Significant monetization possible through debt/equity, debt/debt swaps

Shareholders get benefits of synergies of merger and, potentially, a control premium

Buyer can retain effective control of Board of Directors and senior management of surviving entity, notwithstanding Section 355 requirements

Disadvantages

Monetization limited by market capacity and Section 355 limitations

Limited universe of merger partners due to Section 355 requirement

Post-transaction equity issuance may be limited under Section 355