|

|

Post by Sapphire Capital on Jul 1, 2012 6:48:53 GMT 4

|

|

|

|

Post by ukipa on Jul 2, 2012 20:39:27 GMT 4

They got caught with "their hand in the cookie jar".

|

|

|

|

Post by MMM on Jul 6, 2012 23:01:58 GMT 4

seems they are not the only ones:

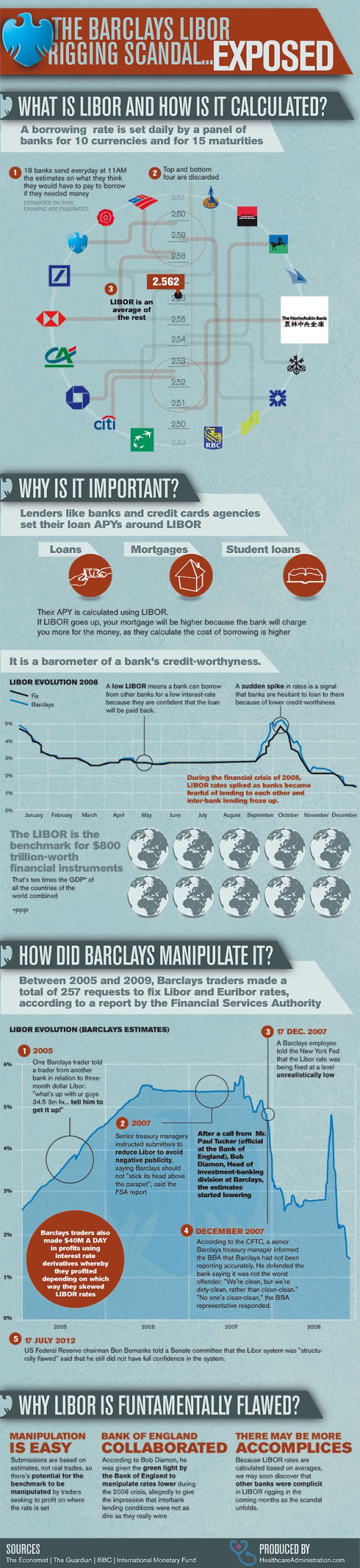

We always knew that the financial markets were rigged, but this is getting ridiculous. It is now being alleged that 20 major banks have been systematically fixing global interest rates for years. Barclays has already been fined hundreds of millions of dollars for manipulating Libor (the London Inter Bank Offered Rate). But Barclays says that a whole bunch of other banks were doing this too. This is shaping up to be the biggest financial scandal in history, and criminal investigations have been launched on both sides of the Atlantic. What those investigations are likely to uncover could shake the financial markets to their very core. In the end, this scandal could absolutely devastate confidence in the global financial system and it could potentially bring down a number of major global banks. We have never seen anything quite like this before.

What Is Libor?

As mentioned before, Libor is the London Inter Bank Offered Rate. A recent Washington Post article contained a pretty good explanation of what that means….

In the simplest terms, LIBOR is the average interest rate which banks in London are charging each other for borrowing. It’s calculated by Thomson Reuters — the parent company of the Reuters news agency — for the British Banking Association (BBA), a trade association of banks and financial services companies.

Why Does Libor Matter?

If you have a mortgage, a car loan or a credit card, then there is a very good chance that Libor has affected your personal finances. Libor has been a factor in the pricing of hundreds of trillions of dollars of loans, securities and assets. The following is from a recent article by Maureen Farrell….

These traders influenced the pricing of the London Interbank Offered Rate or Libor, a benchmark that dictates the pricing of up to $800 trillion of securities (yes trillion)

$800 trillion?

That is a number that is hard to even imagine.

Most American consumers do not even know what Libor is, but it actually plays a key role in the U.S. economy as the Washington Post recently explained….

In the United States, the two biggest indices for adjustable rate mortgages and other consumer debt are the prime rate (that is, the rate banks charge favored or “prime” consumers) and LIBOR, with the latter particularly popular for subprime loans. A study from Mark Schweitzer and Guhan Venkatu at the Cleveland Fed looked at survey data in Ohio and found that by 2008, almost 60 percent of prime adjustable rate mortgages, and nearly 100 percent of subprime ones, were indexed to LIBOR

Who Was Involved In This Scandal?

According to the Daily Mail, in addition to Barclays it is being alleged that at least 20 banks (including some major U.S. banks) were involved in this interest rate fixing scandal….

Hundreds of bankers across three continents are embroiled in the interest-rate fixing scandal that has left Barclays chief executive Bob Diamond fighting to save his job.

As pressure intensified on Britain’s highest paid banking boss to quit, MPs heard a string of other financial institutions across the world were under investigation.

At least 20 banks are believed to be under suspicion, with growing demands for a criminal investigation.

There are also indications that the Bank of England itself may have been involved in this scandal.

What Did They Do?

Employees at Barclays (and apparently at about 20 other major banks) were brazenly manipulating interest rates. A recentYahoo Finance article described how this worked…

To help the bank’s trading positions between 2005 and 2009, and most notably during the global financial crisis of 2007-09, the bank made false submissions to the Libor-setting committee, which agrees rates daily in London.

At the request of its own traders of interest-rate derivatives, Barclays made false submissions relating to Libor and Euribor (the eurozone benchmark rate). By doing this, Barclays personnel aimed to help their trading colleagues to profit by manipulating Libor.

Rigging the world’s leading benchmark for interest rates is pretty serious stuff. Indeed, in the words of the FSA, “Barclays’ behaviour threatened the integrity of the rates, with the risk of serious harm to other market participants”.

Many in the financial world have been absolutely horrified by the details of this scandal that have been emerging.

One recent CNN article declared that “the stench” coming from London is now “overwhelming”….

The Libor scandal has confirmed what many of us have known for some time: There is something smelly in the London financial world and the stench is now overwhelming.

But It is only when I read the Financial Services Authority report — all 44 pages of it — that is became clear just how widespread, how blatant was the fixing of the benchmark interest rate Libor and Euribor by Barclays. Brazen is the only word for it.

The emails and phone calls reveal that on dozens of occasions those who stood to gain by the decisions asked for favors (and got them) from those who helped set the interest rates.

You can read many examples of the kinds of emails that were exchanged between traders in New York and traders at Barclays in London right here.

What Does This Scandal Mean For The Future?

This scandal is making the global financial system look really, really bad. Confidence in global financial markets has already been declining, and these new revelations are not going to help at all. The following is how an article in the Huffington Post put it….

The ballooning interest rate manipulation scandal at Barclays, coupled with stock market instability, is likely to fuel fresh doubts about the integrity of the stock market, insiders said.

“Every time people begin to gain a little confidence, something else comes up,” said Randy Frederick, managing director of active trading and derivatives at Charles Schwab. “If it’s not Europe, it’s [troubled] IPOs, or JPMorgan or Barclays. Something new blows up and people say, ‘I knew it was rigged.’”

In addition, we are undoubtedly going to see a huge wave of lawsuits come out of this scandal. Those lawsuits alone will gum up the financial system for a decade or more.

So needless to say, this is a very big deal.

Sadly, the revelations that have come out about Barclays in recent days are probably just the very tip of the iceberg. Before this is all over, we are probably going to find out that most of the major global banks were involved.

At a time when the global financial system is already on the verge of a major implosion, this is not welcome news.

This financial scandal is just another reason to be deeply concerned about the second half of 2012. The house of cards is starting to look really shaky, and nobody knows exactly when it will fall, but anyone with half a brain can see that things are progressively getting worse.

A “perfect storm” is rapidly developing, and when it strikes it is going to be very, very painful.

|

|

|

|

Post by Money on Jul 17, 2012 21:52:53 GMT 4

Treasury Secretary Timothy Geithner has so far escaped responsibility for the spreading Libor fixing scandal by releasing documents showing that when he became aware of the problem in 2008, as head of the Federal Reserve Bank of New York, he made recommendations to address it.

"The New York Fed analysis culminated in a set of recommendations to reform LIBOR, which was finalized in late May. On June 1, 2008, Mr. Geithner emailed Mervyn King, the Governor of the Bank of England, a report, entitled 'Recommendations for Enhancing the Credibility of LIBOR,'" a Fed statement released Friday reads. "As is clear from the work culminating in the report to Mr. King of the Bank of England, the New York Fed helped to identify problems related to LIBOR and press the relevant authorities in the UK to reform this London-based rate."

With that, Geithner earned a rash of headlines focused on his foresight, as well as criticism for the cozy relationship between regulators and bankers that had led to the controversy.

But the Fed, along with its statement, also released the staff work that led to the recommendations. Those documents reveal that the recommendations Geithner sent to London did not come from staff, but rather were proposed by major banks and more or less forwarded on verbatim.

The policy recommendations Geithner forwarded in an attachment on June 1 first appear in a staff memo dated May 20 that reads: "A variety of changes aimed at enhancing LIBOR's credibility has been proposed by market participants, and seem to be under consideration by the BBA. These proposed changes include, but are not limited to..."

A comparison between Geithner's recommendations and those put forward by "market participants" -- shorthand for banks -- makes it clear that Fed staff asked banks how to fix the problem, then presented those answers as their own.

Source: Huffington Post

|

|

|

|

Post by Melchior on Jul 23, 2012 11:28:59 GMT 4

Prosecutors and European regulators are close to arresting individual traders and charging them with colluding to manipulate global benchmark interest rates, according to people familiar with a sweeping investigation into the rigging scandal.

Federal prosecutors in Washington, D.C., have recently contacted lawyers representing some of the suspects to notify them that criminal charges and arrests could be imminent, said two of those sources, who asked not to be identified because the investigation is ongoing.

Defense lawyers, some of whom represent suspects, said prosecutors have indicated they plan to begin making arrests and filing criminal charges in the next few weeks. In long-running financial investigations it is not uncommon for prosecutors to contact defense lawyers before filing charges to offer suspects a chance to cooperate or take a plea, these lawyers said.

The prospect of charges and arrests means prosecutors are getting a fuller picture of how traders at major banks allegedly sought to influence the London Interbank Offered Rate, or Libor, and other global rates that underpin hundreds of trillions of dollars in assets. The criminal charges would come alongside efforts by regulators to five major banks, and could show that the alleged activity was not rampant at the lenders.

|

|

|

|

Post by Melchior on Jul 25, 2012 11:37:50 GMT 4

|

|

|

|

Post by Bob English on Jul 26, 2012 2:16:58 GMT 4

LIBOR 2.0: Is the Biggest Manipulation Yet to Come? July 25, 2012 By Bob English Economic Policy Journal (http://www.economicpolicyjournal.com/) Is LIBORgate the crime of the century? Or is the real crime yet to come? As has long been alleged at EconomicPolicyJournal.com (http://www.economicpolicyjournal.com/2012/07/difference-between-libor-scandal-and.html), the biggest manipulators of short term rates are the central bankers themselves. Yet, they (unfortunately) have been ignored by the MSM in this mess--even the Bank of England, which appears to be directly culpable (http://www.telegraph.co.uk/finance/newsbysector/banksandfinance/9405197/Libor-emails-show-Bank-of-Englands-efforts-to-get-banks-to-lower-rate.html). Nevertheless, the central banksters,who never let a good [appropriately planned] crisis go to waste, apparently have an even more manipulated scheme to follow. We discussed this [yesterday] on RT's Capital Account with Lauren Lyster (link below), along with a diversion into the timing of the whole LIBOR scandal, which happily coincides with the potential court-ordered (http://www.breitbart.com/Big-Government/2012/07/09/The-Mystery-of-the-Missing-Spitzer-Emails) release of Eliot Spitzer emails that might publicly exonerate Hank Greenberg and AIG (don't worry, CNBC is already on board). If there were ever a moment when Wall Street and DC diverged in recent memory, it is now. Last week, Chairman Bernanke spoke off-the-cuff to the House in a Q&A session and mentioned three potential alternatives to LIBOR. It seems the global central bankers have already planned a September 9th meeting this year to discuss exactly that. And, while details are sketchy at present, whatever replaces the benchmark--to which approximately $500 trillion in notional financial products are pegged--is guaranteed to have the most powerful of influences behind it. According to Bloomberg (http://www.bloomberg.com/news/2012-07-18/central-bankers-to-discuss-libor-s-future-canada-says.html), this meeting, to be headed by Bank of England Governor Mervyn King, will be conducted [behind closed doors], only to be followed up by another [semi-secretive] meeting amongst the policy-makers at the international Financial Stability Board. To date, the only central bankers talking are Bernanke and his Canadian (Bank of Canada Governor) counterpart, Mark Carney. Mr. Carney, echoing Mr. Bernanke, laughably said, "There is an attraction to moving toward obviously [sic] market based rates if possible," he said. Market based indeed. Both Bernanke and Carney mentioned repos (repurchase contracts, presumably of Treasurys/T-Bills) and OIS (overnight indexed swap rates) as replacements, and a third addition by Mr. Bernanke is actual T-Bill rates. Remarkably, there have been few discussions (though see this Stone & McCarthy report at ZH www.zerohedge.com/news/bernankes-libor-alternatives) of this game changing event--which could literally decide the fate of not only money markets themselves, but the life and death of the largest financial institutions (their living wills now cemented in the Eccles Building archives www.bloomberg.com/news/2012-07-02/banks-living-wills-libor-blueprint-china-medical-compliance.html). The principal problem with using either T-Bill or repo rates (or any secured rate, for that matter) is that a premium must be charged. So, who gets to determine the premium? (And, if some other concoction is devised that requires a discount, who determines the discount?) Even if algorithmic in nature, someone must write the algorithm (just as some nameless face wrote the computer program supervised by NYU interns that has bought literally trillions of dollars in securities on behalf of the Federal Reserve). english.economicpolicyjournal.com/2011/01/fil.htmlThe Fed's OIS Conundrum. If one delves into the OIS alternative, even more decidedly non-"market based" potential for manipulation exists. First, OIS is a derivative rate based on an average of the Federal Funds rate--the rate the Fed prefers to manipulate to "target" short term interest rates. However, the "Fed Funds" market is drastically different than years past since the Fed committed to near-ZIRP policy (since December 2008) and since having gained the ability (in October of 2008) to pay banks interest for the money they "keep out of the system" by parking it at the Fed (so-called Interest On Excess Reserves, or IOER). According to the Fed itself (http://www.federalreserve.gov/pubs/feds/2012/201221/201221abs.html), the largest lenders/sellers of Fed Funds are the Federal Home Loan Banks and other GSEs (principally, Freddie and Fannie). This is because, as non-deposit taking institutions, they are not eligible to earn the 0.25% interest the Fed pays to banks. Instead, they earn income on their extra cash by lending it to banks, which, in turn, deposit it at the Fed to collect IOER. Further, according to an email sent by a senior Fed economist to an EPJ reader (http://www.economicpolicyjournal.com/2010/01/blog-post.html), the GSEs prefer to lend only to a few banks (presumably JP Morgan, Goldman Sachs, and the usual suspects). Here is the quote (emphasis ours): Anecdotal evidence suggests that all of the housing-related entities are willing to lend to the same few banks, which limits the possibility for competition to raise market rates. Thus, a LIBOR "alternative" that uses the OIS rate as its substitute switches from (a) an average of declared rates by 14 or so banks to (b) an average Fed Funds rate determined by back-door dealings between the largest government sponsored failures (GSFs?) in history and the compromised TBTF banks with whom they prefer to transact. At least the Fed (and the administration) can sleep knowing this scheme limits competition to push rates to the upside. None of this is to discount the fact that the large banks wantonly manipulated LIBOR for their own gain on a day to day basis. Nor are we are not attempting to mitigate their culpability for such. Were we given the chance to indict the banksters for LIBOR or for nothing at all, guess which we would choose (though, we'd insist throwing Corzine in for good measure). The point is that after all the show trials and show hearings on LIBOR, all we are guaranteed is that the central planning oligarchy will have its tentacles more firmly entrenched in its manipulation scheme of the entire finance sector. The question is only which power centers will be directing the circus. (http://www.economicpolicyjournal.com/2009/12/you-have-to-understand-power-centers.html) |

|

|

|

Post by Hans on Aug 2, 2012 21:54:08 GMT 4

Li(e)bor: The Cartel Emerges

August 1, 2012

Source: Zero Hedge

Just when you thought the Li(e)bor scandal had jumped the shark, Germany's Spiegel brings it back front-and-center with a detailed and critical insight into the 'organized fraud' and emergence of the cartel of 'bottom of the food chain' money market traders. "The trick is that you can't do it alone" one of the 'chosen' pointed out, but regulators have noiw spoken "mechanisms are now taking effect that I only knew of from mafia films." RICO anyone? "This is a real zinger," says an insider. In the past, bank manager lapses resulted from their stupidity for having bought securities without understanding them. "Now that was bad enough. But manipulating a market rate is criminal." A portion of the industry, adds the insider, apparently doesn't realize that the writing is on the wall.

There have been plenty of banking scandals, but none quite like this: Investigators and political leaders believe that the manipulation of the Libor benchmark interest rate was the result of organized fraud. Institutions that participated could face billions in fines and penalties.

SPIEGEL: The Cartel Emerges

In 2005, a young trader with Moroccan roots came to Barclays: Philippe Moryoussef, who is now 44... Moryoussef traded in interest rate derivatives during his time at Barclays. He and his fellow traders knew exactly how much money they stood to lose or gain if the Libor or Euribor changed by only a fraction of a percentage point in one direction or the other.

And they apparently did everything they could to eliminate happenstance. Moryoussef communicated by phone or email with colleagues inside and outside the bank almost daily to steer interest rates in the right direction. To do so, they sent inquiries to the people who were responsible for inputting the Libor rates: the money market traders.

In the glitzy world of investment banking, money market traders were at the bottom of the pecking order before the financial crisis. They were not involved in major deals, and they could only dream of the kinds of bonuses stock and bond traders received. "They were always at the bottom of the food chain," says a former investment banker.

It was a conspiratorial group of underdogs who worked for various banks and met at least once a month for a beer or a mojito in New York, London or Frankfurt. By the middle of the last decade, when there seemed to be a surplus of money at the banks, they all had the same problem: They were derided or, worse yet, ignored by their colleagues in the trading rooms of major banks.

But what if it were possible to know where interest rates were headed at the end of the day, or even in the next hour? What if a few traders could manipulate the ups and downs of interest rates?

By 2005 at the latest, the traders would seem to have begun realizing just how much power they had were they able to collaborate within their small group. There was no need for formal contracts between large institutions, merely agreements among friends. A pointer here, a few traders meeting for lunch there, and soon the group had formed a global cartel that, according to investigators, reached from Japan to Europe to Canada.

"Come on over; I'll open a bottle of Bollinger," a trader, inebriated with his success, wrote to a colleague after the Libor rate had been set. Adair Turner of the British regulatory agency quotes the email as evidence of "a culture of cynical greed in the trading rooms."

The Organized Fraud

"If the rate remains unchanged, I'm a dead man," a trader emailed to a colleague who was responsible for Libor in October 2006. The traders sent at least 173 inquiries of this nature between 2005 and May 2009 for the dollar Libor alone. They were often successful.

"The trick is that you can't do it alone," he bragged to outside colleagues at HSBC, Société Générale and Deutsche Bank, who allegedly cooperated with him.

While the traders were initially out to increase their bonuses, the manipulation took on a different dimension during the crisis. When the first banks began to wobble in 2007, it became more difficult for many financial companies to borrow money -- a problem that would normally be reflected in higher Libor rates.

Now even top managers at Barclays, alarmed by media reports, were instructing the Libor men to input lower rates. In October 2008, the manipulation became a question of survival for Barclays. On Oct. 29, a concerned Paul Tucker, now the deputy governor of the Bank of England, contacted Barclays CEO Diamond. Tucker wanted to know why the bank was consistently inputting such high interest rates into the daily Libor report.

Diamond told a parliamentary committee that Tucker had suggested to report lower interest rates for the Libor, which Tucker staunchly denies. Diamond, for his part, prepared a transcript of the telephone conversation he had had with Tucker on that day, in which he had mentioned political pressure. After that, his chief operating officer spoke with the money market traders. The underdogs were suddenly being heard on the executive board, and had become the bank's potential saviors.

Barclays wasn't the only bank that was having trouble gaining access to money in the fall of 2008. UBS, Citigroup and the Royal Bank of Scotland, now prime suspects in addition to Barclays, had to be bailed out by their respective governments. Germany's WestLB, which was involved in the Libor calculation at the time, was also seen as a problem case, although this wasn't reflected in the Libor rates it was reporting.

...

The Failure of the Regulators

On April 11, 2008, a member of the Barclays money market team called Fabiola Ravazzolo, an employee of the Federal Reserve Bank of New York.

Barclays employee: "LIBORs do not reflect where the market is trading, which is, you know, the same as a lot of other people have said."

Ravazzolo: "Mm hmm."

A few moments later, the Barclays man, according to the transcript of the conversation released by the bank, said: "We're not posting, um, an honest Libor."

Ravazzolo: "Okay."

Barclays-Mann: "We are doing it, because, um, if we didn't do it it draws, um, unwanted attention on ourselves."

Ravazzolo: "Okay."

There was no sense of outrage, nor did Ravazzolo question the Barclays employee about the details. A similar conversation transpired with another Fed employee a few months later.

These are transcripts of failure...

Meanwhile, the US Commodities Futures Trading Commission (CFTC) had been investigating the issue since 2008, and its efforts eventually led to a worldwide investigation.

The Episode Is Blown Wide Open

"Mechanisms are now taking effect that I only knew of from mafia films," a shaken financial regulator said recently. Since investigations have gone into high gear in New York, London, Brussels and elsewhere, suspected bank executives have been coming clean.

They are under great pressure. Last year, the European Commission filed several antitrust suits against various banks. Antitrust suits are considered to be the sharpest weapons in business law because they allow Brussels to impose stiff penalties on cartel participants.

"In our investigations, we concentrate on suspicious cartel agreements that include derivatives. This includes possible secret agreements about the determination of these lending rates," says European Competition Commissioner Joaquín Almunia. In other words, the investigators are interested in more than the manipulation of global interest rates to benefit specific parties. It's also possible that the enormous market for derivatives was manipulated.

"Derivatives traders are also believed to have agreed upon the difference between the buy and sell prices (spreads) of derivatives, thereby selling these financial instruments to customers under conditions that were not customary in the market," says the Swiss Competition Commission, which is also investigating possible cartels.

It is difficult to find clear evidence, such as a written cartel agreement. But in Brussels alone, more than 40 banks have contacted authorities to report what they know about years of manipulation...

What the Banks Could Now Face

German banks must have pricked up their ears when BaFin President Elke König recently spoke about the Libor scandal. "Basically, banks must establish suitable reserves for possible losses," König concluded.

Investors, like Vienna hedge fund FTC Capital, have made it clear that they do not intend to let up. They feel obligated to their customers to file claims for damages, explains FTC executive Majcen...

There are already 20 lawsuits in the United States, some of which have been combined into class action suits. The plaintiffs range from the City of Baltimore to police and firefighter's pension funds, the City of Dania Beach, Florida, and Russian oligarch Vladimir Gusinsky.

They feel encouraged by the actions of regulators. "Both the American CFTC and the FSA have done excellent investigative work," says Majcen. Bank analysts expect that other institutions could face fines similar to the one imposed on Barclays. In fact, it ought to be in the banks' best interest to quickly settle their cases. "But they're afraid, because since Barclays, they know that it isn't just about money, but also about making heads roll," says a major shareholder of Deutsche Bank.

German attorneys are also lining up to represent potential clients. "A few institutional investors have already contacted us," says Marc Schiefer of the law firm TILP in the southern German city of Tübingen.

Years could go by before damage suits are ruled on...

Possible Libor-related liabilities would cause serious problems at WestLB, or its successor company Portigon. The once-proud state-owned bank is in the process of being liquidated, at a cost of billions to its former owners, the western German state of North Rhine-Westphalia and savings banks. The Libor scandal could further increase the burden on taxpayers.

...

The call for stricter regulation is also getting louder in politics once again... "cheap populism."

"This is a real zinger," says an insider. In the past, bank manager lapses resulted from their stupidity for having bought securities without understanding them. "Now that was bad enough. But manipulating a market rate is criminal." A portion of the industry, adds the insider, apparently doesn't realize that the writing is on the wall.

The parties involved, including Deutsche Bank and its new co-CEO Jain, cannot expect leniency when charges are investigated. "We can't make any allowances for high-profile names," say officials in the capital.

|

|